The Bureau of Internal Revenue (BIR) provides clarification on what qualifies as an allowable or deductible business expense for tax purposes. For many businesses and professionals, determining which expenses can legally reduce taxable income can be confusing. RMC No. 81-2025 reiterates that only expenses that are ordinary, necessary, reasonable, and directly related to the operation of the business, and supported by proper documents, may be claimed as deductions. Understanding these guidelines help taxpayers ensure compliance, maintain accurate records, and avoid issues during tax assessments or audits.

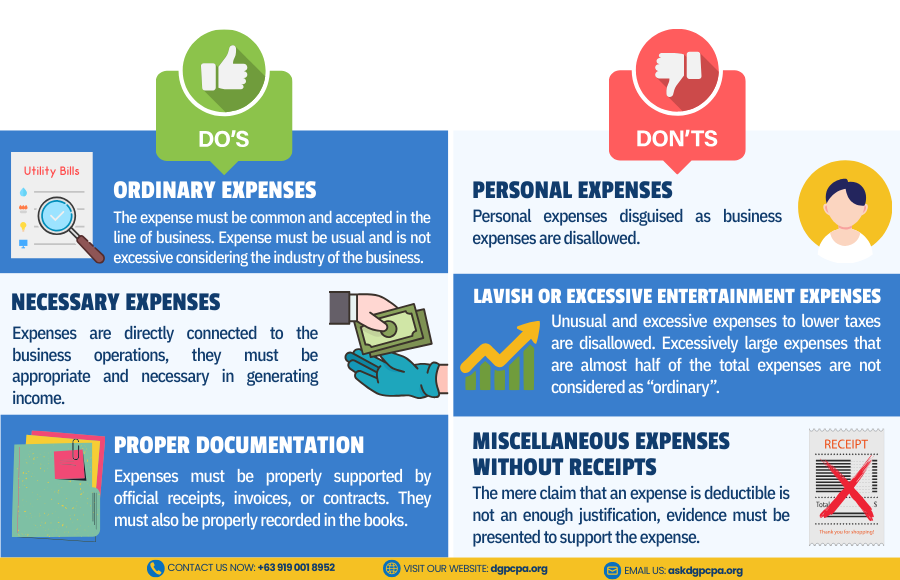

To reinforce the important rule in taxation: not all business expenses are automatically deductible. We are again reminded that only expenses that are considered ordinary and necessary in the conduct of business may be claimed as deductions from gross income.

To qualify as deductible, an expense must be ordinary, meaning it is common and accepted within the taxpayer’s industry or line of business. These are the usual costs that businesses typically incur in their daily operations, such as rent, utilities, and salaries. The expense should be reasonable in amount and consistent with normal business practices. In other words, it must be something that similar businesses would normally spend money on as part of their operations. On the other hand, a necessary expense has a clear connection to the business and contributes to generating income. While the expense does not have to be indispensable, it must be appropriate and helpful in carrying out the business’ activities. Expenses that support operations, improve efficiency, or enable the business to operate effectively may generally fall under this category.

Aside from meeting the “ordinary and necessary” test, it is also emphasized by the circular the importance if proper substantiation. Taxpayers must be able to prove that the expense was actually incurred and is directly related to the business. This requires maintaining adequate documentation such as sales invoices, contracts, and properly recorded entries in the books of accounts. Proper documentation not only supports the legitimacy of the expense but also helps taxpayers defend their deductions during tax audits or assessments.

The circular also reminds us what expenses could be considered as red flags during tax audits or assessments. These include personal expenses that are incorrectly claimed as deductions, lavish or excessive entertainment expenses, and miscellaneous expenses that lack sufficient supporting documents. Such items may be disallowed as deductions, resulting in adjustments to taxable income.

Ultimately, RMC No. 81-2025 serves as a reminder for businesses and professionals to exercise diligence in recording and claiming their expenses. Proper classification, documentation, and adherence to tax regulations are essential in ensuring compliance. BY understanding and applying these guidelines, taxpayers can avoid disallowed deductions, potential tax deficiencies, and penalties, while maintaining transparent and accurate financial records.

![]() Source: BIR Memorandum Circular No. 81, Series of 2025.

Source: BIR Memorandum Circular No. 81, Series of 2025.

![]() View the full document here: https://bir-cdn.bir.gov.ph/BIR/pdf/RMC%20No.%2081-2025.pdf

View the full document here: https://bir-cdn.bir.gov.ph/BIR/pdf/RMC%20No.%2081-2025.pdf

Disclaimer:

The information provided herein is intended for general informational purposes only and reflects the current understanding of the given topic. It is subject to change in response to updates in laws or regulations. This material does not constitute legal or financial advice. For tailored advice, please contact De Guzman Pascual and Associates CPAs at [email protected]. The views expressed do not necessarily represent any official position of governmental or financial entities.